2025 Residential Construction Industry Outlook

As we look toward the remainder of 2025, the home building and renovation industry finds itself at an interesting crossroads. Despite facing significant headwinds in 2024, the latest Houzz State of the Industry report reveals a surprisingly optimistic outlook among construction and design professionals. This resilience, contrasted against last year’s challenges, offers valuable insights into where our industry is headed.

Looking Back: The Challenging Landscape of 2024

The data tells a clear story: 2024 was tough for virtually everyone in the construction and design sectors. Revenue declined across all seven industry groups tracked by Houzz, marking the largest year-over-year dip since 2014. Specialty interior services were hardest hit with a 7.2% revenue decline, followed by landscaping and outdoor service firms at 6.5%. Even traditionally stable sectors weren’t immune, with interior designers experiencing a 4.1% revenue drop and architects seeing a 2.4% decrease.

Profitability also suffered significantly. Between 44% and 60% of firms across all industry categories reported decreased profits in 2024, compared to just 23% to 39% the previous year. This downturn coincided with widespread increases in the cost of doing business, with 65% to 81% of firms reporting higher operational costs.

The primary culprits behind these rising costs were:

- Material prices: For six of the seven industry groups, rising product and material costs contributed most significantly to increased expenses

- Business insurance: Consistently ranked among the top three cost drivers

- Labor costs: Both direct employee wages/benefits and subcontractor costs put pressure on margins

These challenges weren’t occurring in isolation. The building industry has been wrestling with the compounding effects of tariffs on essential building materials. According to the National Association of Home Builders (NAHB), tariffs on Canadian lumber alone have added thousands of dollars to the cost of an average single-family home. Additional tariffs on steel, aluminum, and various imports from China have further strained the supply chain and increased costs.

The Surprising Optimism for 2025

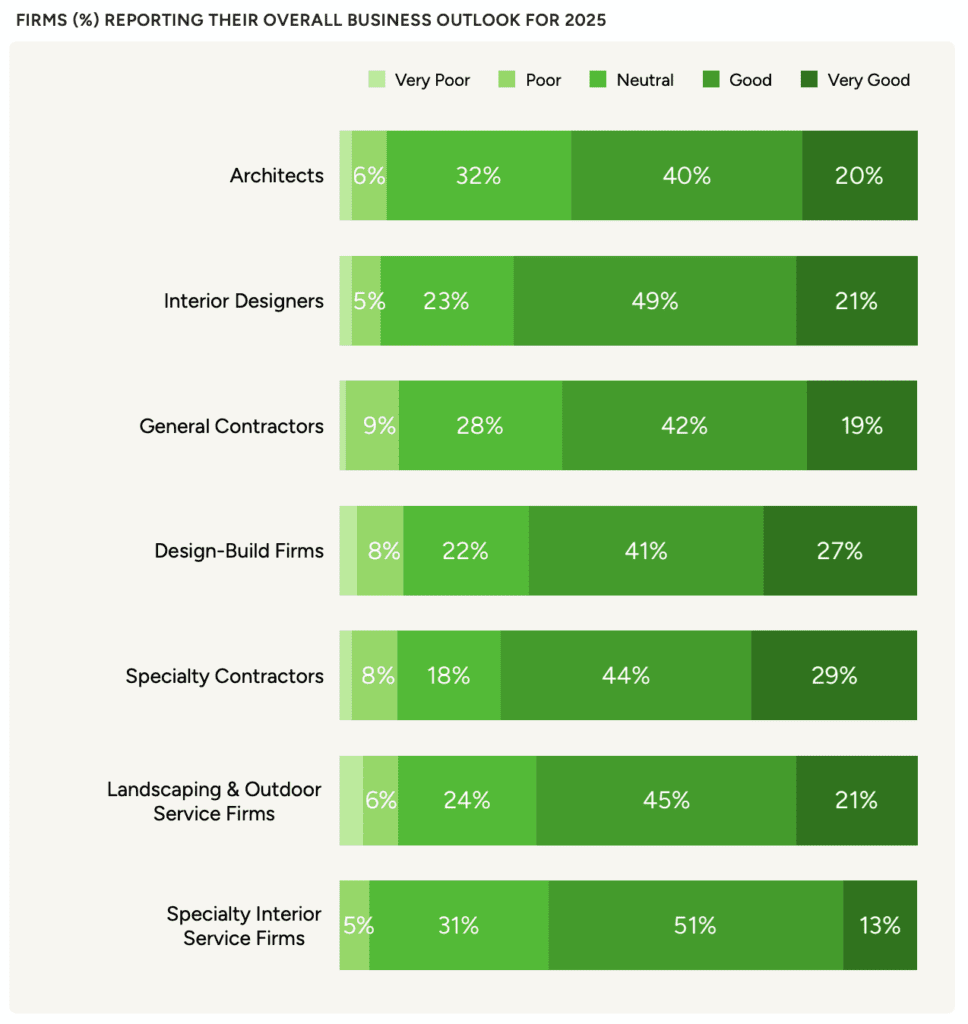

What makes the current landscape so interesting is the contrast between these recent difficulties and the widespread optimism for 2025. More than three in five firms across all sectors report a positive business outlook:

This optimism extends to revenue projections as well. Construction businesses anticipate impressive double-digit growth in 2025, with specialty contractors expecting 12.4% growth and general contractors projecting 11.3%. Design professionals are also bullish, with architects anticipating 9.4% growth and interior designers projecting 9.0%.

What’s Driving This Confidence?

Several factors were cited to be fueling this positive outlook:

- Expanding service offerings (21-57%)

- Anticipated economic improvement: More firms expect both the national and local economies to improve than expect them to worsen

- Increased demand: Between 51% and 77% of businesses across all groups anticipate higher demand for services in 2025

- Strategic adaptations: Firms are implementing various strategies to drive growth, including: Targeting larger-budget projects (54-74% of firms depending on category), Increasing prices, markups and margins (42-57%), Improving sales processes (22-44%).

Challenges That Remain on the Horizon

Despite the optimism, significant challenges persist:

- Labor concerns: More firms expect labor availability to worsen (29-46%) than improve (13-19%),

- Rising costs: 51-57% of businesses across six industry groups expect labor costs to increase further,

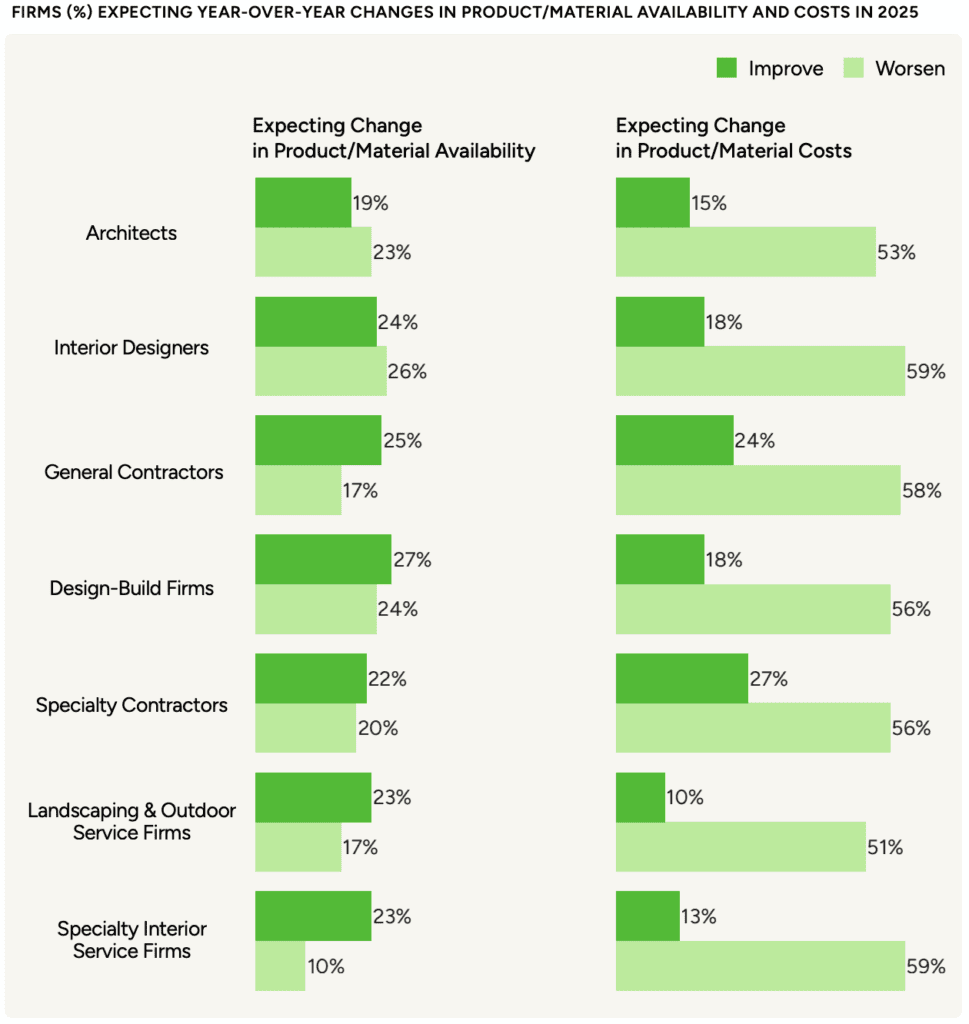

- Material costs: The majority of firms across all seven groups expect product and material costs to continue rising,

- Client acquisition: Finding prospective customers was cited as a top challenge, particularly for interior designers (43%), specialty interior services (37%), and architects (32%).

The ongoing impact of tariffs and trade policies on building materials remains a wild card. While these policies aim to protect domestic industries, they’ve had significant downstream effects on construction costs. According to NAHB analysis, tariffs have affected approximately $10 billion in goods used by the residential construction industry at the date of publication.

“NAHB estimates that $204 billion worth of goods were used in the construction of both new multifamily and single-family housing in 2024. $14 billion of those goods were imported from outside the U.S., meaning approximately 7% of all goods used in new residential construction originate from a foreign nation.”

Tariffs remain an unknown with a potentially significant impact when you look at the imports the U.S. receives from abroad. According to NAHB:

- Of $8.2 billion worth of sawmill and wood products imported in 2024, nearly 72% of these imports came from Canada. Total imports of sawmill and wood products from Canada totaled $5.9 billion.

- The U.S. imported $481 million worth of lime and gypsum products in 2024, with 74% of these products originating from Mexico. Imports of lime and gypsum products from Mexico totaled $354 million in 2023.

The proposed tariffs are on top of existing 14.5% lumber tariffs previously imposed by the U.S. Department of Commerce. The Department of Commerce has also signaled an intent to double these tariffs. This, coupled with the proposed tariffs mean softwood lumber imported from Canada could have a 50% – 60% total tariff imposed on it.

Overall, the proposed new tariffs on China, Canada and Mexico are projected to raise the cost of imported construction materials by more than $3 billion, depending on the specific rates.

Looking Ahead: Navigating 2025 and Beyond

As we move through 2025, successful firms will need to balance optimism with practical strategies for addressing persistent challenges. Those who can effectively manage rising costs, improve client acquisition methods, and leverage technology to enhance efficiency will be best positioned to capitalize on the anticipated growth.

The residential market, particularly projects involving existing homes, continues to be the primary revenue driver across all industry groups. This suggests that renovation and remodeling, rather than new construction, may offer the most stable opportunities in the near term.

Despite headwinds from economic uncertainty, material cost volatility, and labor challenges, professionals across the construction and design spectrum are finding ways to adapt and even thrive.

As the year progresses, Casper Builders will continue monitoring these trends to see if this optimism translates into the projected growth. In the meantime, focusing on efficiency, client relationships, and strategic pricing is the approach for navigating the complex landscape ahead.